Authorized Push Payment (APP) Fraud

Authorized Push Payment (APP) fraud tricks you into willingly sending money to scammers. It appears authorized since you initiate it, despite false/misleading info.

What Is Authorized Push Payment (APP) Fraud?

Authorized Push Payment (APP) fraud is a type of financial scam where a person is manipulated into willingly sending money to a scammer, believing the payment is legitimate. Because the victim authorizes the transfer themselves, the payment often bypasses standard fraud protections and can be difficult to recover.

APP fraud is defined by how the payment happens, not just by deception.

In an APP fraud scenario, the victim:

- Initiates the payment personally

- Uses a real bank transfer or payment app

- Believes they are protecting their money or resolving a legitimate issue

From the bank’s perspective, the transaction looks “authorized,” even though it was the result of manipulation. This distinction is why APP fraud is treated differently from unauthorized account theft.

How APP Fraud Happens in Real Life

APP fraud usually begins with false but convincing instructions about money movement.

A scammer may claim:

- There is fraud on your account and money must be moved immediately

- Your bank has seemingly created a “safe” or “temporary” account

- A payment is required to stop further losses or secure funds

- A trusted contact needs urgent financial help through a transfer

The request often comes through a phone call, text, or message that appears to be from a legitimate source, such as a bank employee or company representative. The pressure is not accidental—scammers rely on stress and urgency to prevent verification.

Why APP Fraud Is Especially Dangerous

APP fraud is one of the most financially harmful scam categories because it exploits how modern payment systems work.

Key risks include:

- Limited reimbursement: Because the victim authorizes the payment, banks may not automatically refund the loss.

- Fast, irreversible transfers: Payments sent via wire transfer, peer-to-peer (P2P) apps, or instant bank transfers are often difficult to reverse.

- High-pressure manipulation: Victims are often coached step-by-step to complete the transfer without consulting others.

Regulators and consumer protection agencies have identified APP fraud as a growing concern precisely because it sits in the gap between “authorized” and “fraudulent.”

Common APP Fraud Scenarios

APP fraud frequently appears in connection with real payment tools and institutions, including:

- Peer-to-peer payment scams: Requests to send money via Zelle, Venmo, or similar services to stop fraud or resolve an account issue.

- Bank transfer scams: Instructions to move funds to a new account that is falsely described as secure or temporary.

- Imposter-driven payment requests: Scammers posing as banks, employers, or vendors directing victims to authorize urgent transfers.

- Invoice or payment diversion scams: Fake payment instructions that redirect legitimate payments to a scammer-controlled account.

How to Tell If a Payment Request May Be APP Fraud

A payment request may involve APP fraud if:

- You are told to move money quickly to prevent loss

- The request involves a new or unfamiliar account

- You are instructed not to speak with others

- Verification is discouraged or delayed

- The payment is framed as the only way to protect your funds

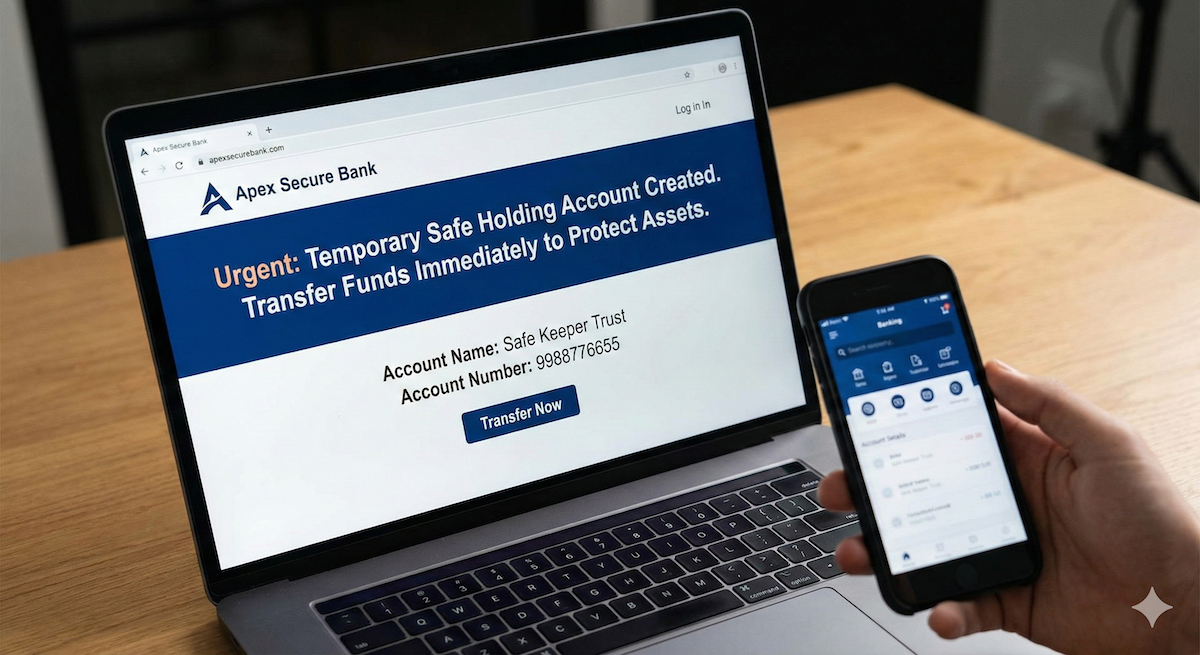

Legitimate banks do not ask customers to move money to “safe” accounts over the phone or by message.

How to Protect Yourself from APP Fraud

Protecting yourself from Authorized Push Payment (APP) fraud starts with understanding a key principle: once you authorize a payment, banks may have limited ability to reverse it. That’s why prevention matters more than recovery.

1. Slow down any request to move money

APP fraud depends on speed. Scammers create situations where moving money feels like the only way to stop a problem. Legitimate banks do not require immediate transfers to protect your funds. If you’re told you must act “right now,” that’s a reason to pause—not comply.

2. Don’t trust inbound payment instructions

Calls, texts, or emails that instruct you to send money—even if they appear to come from your bank—should not be treated as verification. Scammers can spoof phone numbers and impersonate real institutions.

If a payment is truly required, you should be able to confirm it by initiating contact yourself using a phone number or website you already trust.

3. Never send money to a “safe,” “temporary,” or “holding” account

Banks and payment providers do not use customer-directed “safe accounts” to stop fraud. Any request to move money to a new or unfamiliar account—especially one you didn’t set up yourself—is a strong indicator of APP fraud.

4. Treat payment apps like cash

Peer-to-peer payment tools and bank transfers are designed for speed and convenience, not dispute resolution. Once money is sent, it may be gone. Only send payments when:

- You fully understand why the payment is needed

- You recognize the recipient

- You’ve independently verified the request

5. Add a second checkpoint before sending money

Before authorizing any urgent transfer, involve another person—a family member, caregiver, or trusted advisor. APP fraud often works because scammers isolate victims during the decision. Breaking that isolation reduces risk immediately.

6. If money has already been sent, act quickly

If you realize a payment may have been part of APP fraud:

- Contact your bank or payment provider immediately using official contact information

- Ask about transaction recalls or fraud escalation options

- Consider reporting the incident to the FTC or FBI’s Internet Crime Complaint Center (IC3)

You can also use a trusted free scam checker like Scamwise to review suspicious payment requests before taking action.

FAQs

What is Authorized Push Payment (APP) fraud?

APP fraud happens when someone is tricked into sending money themselves, believing the transfer is legitimate, even though it was based on false information.

Why is APP fraud hard to recover from?

Because the victim authorizes the payment, banks may treat it differently from unauthorized fraud, making refunds more difficult.

Do banks ever ask customers to move money to a safe account?

No. Legitimate banks do not instruct customers to move money to separate accounts to prevent fraud.

What should I do if I think I’m being pressured into sending money?

Stop, end the interaction, and contact your bank directly using official contact information before taking any action.

You can't always be there. Savi can.